Principles applied

There are five principles that support the development of our costing model:

- Linked to strategic business planning: costing is not just a ‘bean counting’ exercise. It should be linked to the strategic direction and planning of AMSA and inform executive at a strategic and tactical level.

- Holistic approach: a modelling exercise should include all revenue and operating expenditure, including overheads, other indirect costs, and capital expenditure (capital allowances and/or depreciation). Further, it should focus not just on cost recovery activities, but all activities of AMSA. This will result in a model that can fulfil multiple demands for costing information.

- Comprehensive and consistent: a simple approach that applies consistency in the application of modelling rules across all business areas and activities, creating a robust model understood by stakeholders. It should be developed over short timeframes, with a relatively small input of resources.

- Flexibility: it is important to recognise that demands for service delivery change over time, driven by various internal and external circumstances. A costing exercise must be dynamic in nature to evolve with changes to AMSA’s business requirements and circumstances.

- Institutionalised as a ‘normal’ function: modelling should be a living database that requires regular updating on a periodic basis. This is successful when the model receives official endorsement with AMSA wide involvement (operational area’s ‘buy-in’). Costing will then become a routine task and a ‘foundation stone’ for improving and reporting on financial performance.

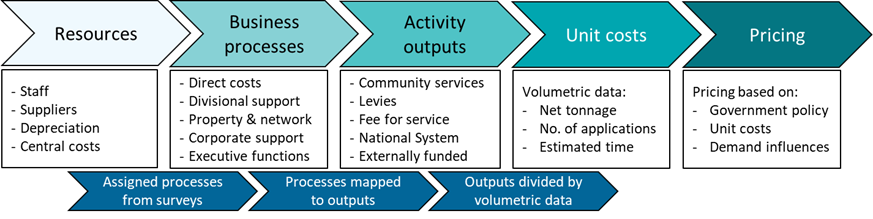

Methodology

The methodology for modelling AMSA’s costs is summarised in the illustration below. It adheres to activity-based costing principles, which enables more analysis on the efficiency of activity outputs and/or business processes for cost recovery and other activities. It focuses on cost drivers, which allocates indirect costs to direct costs and then to an output.

Not all business processes are specific or direct in the provision of activity outputs. Several tasks are support related activities that simply enable the delivery of AMSA’s core outputs to stakeholders. Nevertheless, these should form part of the activity cost.

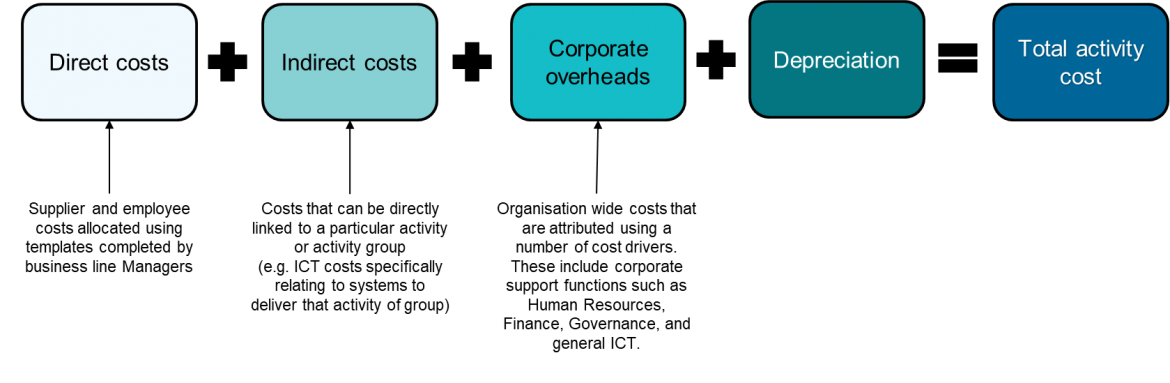

Cost categories

As part the costing methodology, we assign each activity to one of the following four cost categories to ensure appropriate identification of overheads for allocation to an activity.

- Direct: representing direct business processes (or tasks) relevant in-service delivery of activity outputs.

- Indirect: exists to support the delivery of a direct activity. Examples include divisional support activities such as general management, specific ICT costs relating to systems to enable service delivery, and supporting property operating expenditure, ICT networking, and communication. Indirect processes are allocated to direct activities based on a cost object using an appropriate driver.

- Corporate overheads: enabling tasks and activities to support service delivery of AMSA’s activity outputs through provision of standard corporate and executive functions. Corporate overheads include executive, human resources, finance, governance, and general ICT support, accompanying their respective share of property operating expenditure, ICT networking, and communication. Like indirect, corporate overheads allocated to direct activities based on cost drivers.

- Depreciation: representing capital costs, asset register assessed on an asset-by-asset basis. Where there is a specific direct link to an activity, depreciation is assigned to an activity group, where corporate support related, depreciation is assigned to the appropriate overhead classification.

Below is an outline of the composition of an activity cost.